Latest Breaking News Online News Portal

Latest Breaking News Online News Portal

High Street banks are facing demands to offer higher interest rates to their loyal savers (Image: GETTY)

High Street banks are facing demands to offer higher interest rates to their loyal savers.

Industry regulators should make High St giants improve “meagre” and “unjustifiably low” interest payments, say experts.

Some banks are accused of “ripping off” savers by hundreds of pounds a year as customers are reluctant to leave big-name businesses in order to seek better rates at lesser-known “challenger” brands.

Observers point out that historically low interest rates have been rising but banks have in turn failed to give customers higher returns on their nest eggs.

A Which? survey reveals that a saver with £10,000 to invest can be left up to £312 a year worse off if they stick with traditional brands – some rates were as low as 0.1 percent.

READ MORE: Ex-Bank of England chiefs warning of huge interest rate hike

The Bank of England raised its base interest rate to 4.5% (Image: GETTY)

Angry ex-pensions minister Sir Steve Webb called for “effective and enforced action by regulators” to force banks to improve their offer to savers. He added that the High Street businesses “are just taking advantage of people”.

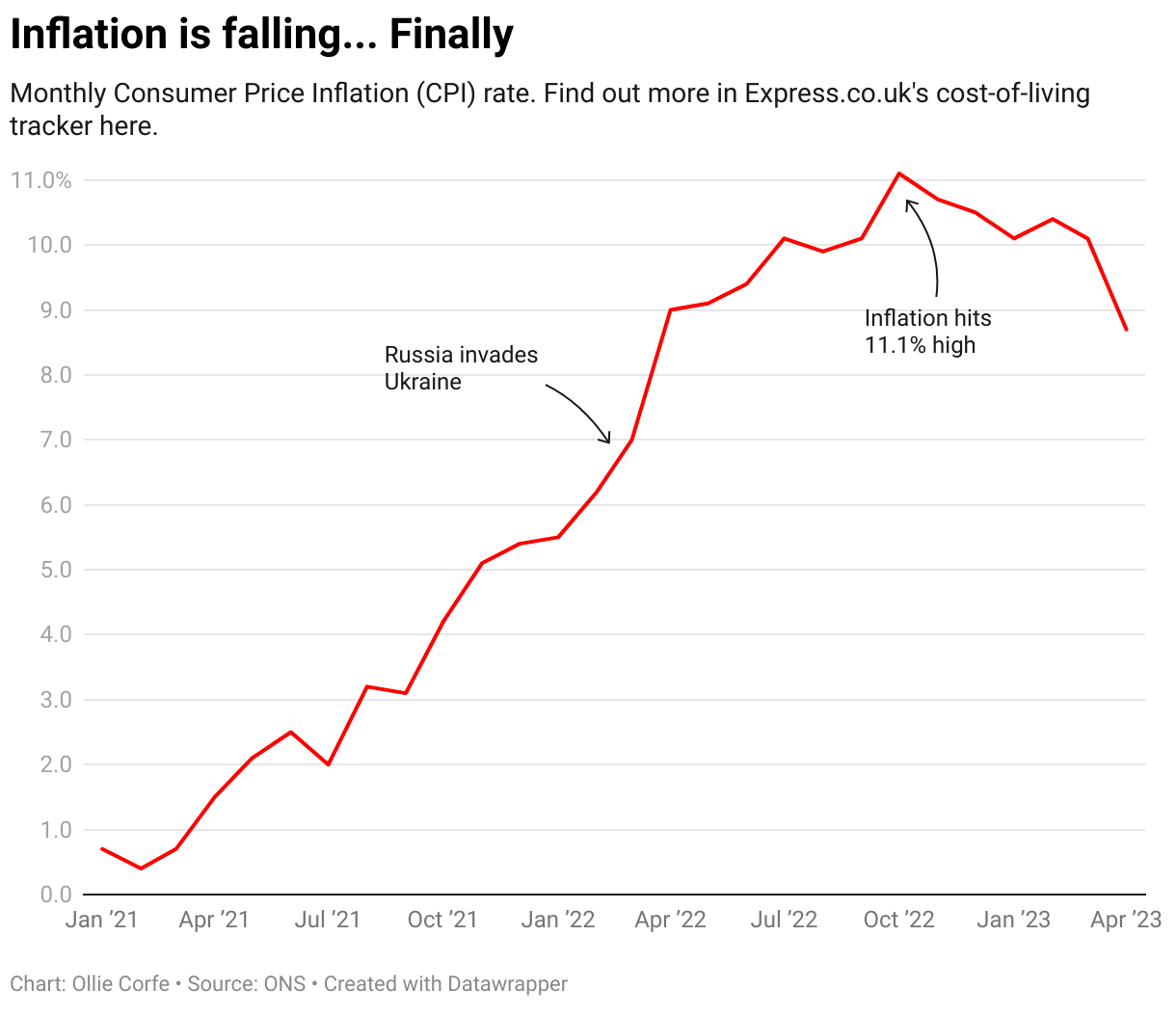

A spokesman for Which? said of the low returns on savings: “Such measly rates are unjustifiable, particularly at a time when borrowers are being hit with higher repayments and the Bank of England rate is now 4.5 percent.

“Our advice is simple: if you’re not satisfied with the rates you’re currently receiving, now’s the time to switch.”

Sir Steve said: “Savers have had their savings ravaged by inflation in the last couple of years. A lot of people have a little nest egg, maybe in cash or in an ISA.

“The only thing that’s on your side is the interest that you receive. Cash rates of interest have been appalling for years. Now that rates are rising, there’s really just no excuse for savings rates not to rise. And I think that banks are just taking advantage of people.

“People don’t spend their life checking rate comparison tables, they don’t spend their life switching accounts to get the best rate – and the banks know that.

“They know they can get away with this. The losers are not the well-advised, the well-informed and the well-off. It’s ordinary savers who’ve put a bit of money to one side, have been hit hard by inflation and now don’t even get the upside when interest rates are going up.”

Many of the banks’ most loyal customers are older people (Image: GETTY)

Sir Steve said that he believed major banks would never voluntarily offer better value – and so they needed to be compelled to do so.

He added: “I certainly feel we’ve been talking about this for what feels like forever. And nothing ever seems to change. The banks will only act when they’re made to act. They’ve realised that if they just drag their heels, do nothing, there’ll be another report and another shot across the bows and nothing will happen.”

He said it would be impossible to legally bind interest rates offered to savers to the Bank of England base rate – but the situation “certainly needs…effective and enforced action by regulators.

“Clearly, threats have achieved nothing, we need effective measures so that savers get a fair deal.”

He added the Financial Conduct Authority and the Treasury were the regulators best placed to compel the banks to change.

Many of the banks’ most loyal customers are older people who are less likely to switch brands in pursuit of better returns.

Caroline Abrahams, charity director at Age UK, commented: “There are rarely benefits from being a loyal customer these days and it usually pays to shop around for financial services.

“However, that’s much easier to do if you have access to the internet and we know that millions of over-65s are not online.

“These findings are a useful reminder for anyone in that position, and indeed the rest of us too, not to assume that we’ll get the best deal if we stick with our current provider.” Last month the FCA said it will use tougher consumer protection powers to ensure banks pass on rate rises to savers.

This will happen as it begins phasing in consumer duty rules from July 31, giving it stronger powers to ensure that the firms which it regulates are acting in the best interest of their customers.

The Treasury Select Committee of MPs recently asked Nationwide, Santander, TSB and Virgin Money why their rates were so low.

Harriett Baldwin MP, chair of the committee, said at the time: “Recent results show that the UK’s biggest banks are continuing to squeeze record profits from their loyal savers. In a high interest rate environment – and with further Bank of England base rate rises possible – banks must do more to encourage saving.

“We would like to know why savings rates offered by banks and building societies are so much lower than the current base rate, and whether banks tell their loyal customers better deals could be available. We are concerned that the loyalty penalty may be particularly severe for elderly or vulnerable customers who may not be able to take advantage of higher rates available online.

“Consumers should continue to vote with their feet and find better offerings. This, more than anything, will drive the banks to increase their currently measly rates.”

A spokesman for banking trade association UK Finance said: “The rates an individual firm offers on its savings products are driven by a number of different factors, not just the Bank of England’s bank rate. One important factor is whether someone wants instant access or can deposit their money for a longer period of time.

“While the interest rate on an instant access account may be lower, they offer customers the flexibility to access their money when they need it.

“The market is competitive with a range of fixed and variable rate products available.

“We would always encourage customers to shop around for the product and interest rate that is suited to their needs.”

COMMENT BY JENNY ROSS

Our research today paints a bleak picture of just how meagre savings rates offered by some of the biggest banks in the country have been recently.

Taking data from the last three years, we’ve found just how far traditional high street names lag behind challenger banks when it comes to rates on a range of savings accounts and Isas.

Whether it’s instant access savings or Isas, or fixed-rate deals over one or five years, we’ve found some paltry rates on offer.

Take, for instance, Barclays’ Everyday Saver or Lloyds’ Easy Saver instant access savings accounts, which both offered rates of just 0.1 percent between January 2020 and March 2023. Contrast that with challenger banks’ average rates over the past three years – 0.57 percent – and it becomes clear that customers of high street banks have been consistently short-changed.

Despite the Bank of England raising interest rates, banks don’t seem to have got the memo that they can pass on those rates. With inflation still stubbornly high, which eats away at the value of our savings, it’s vital consumers get the best rates possible.

We aren’t the only ones to question the approach of big banks. The Treasury Select Committee recently wrote to high street banks asking them to lay out how they decide what level of savings rates to pass on to savers, and whether they let customers know that higher alternatives may be available.

Back in 2018, regulator the Financial Conduct Authority, did consider introducing a single rate for savers who had been with their provider for over 12 months.

The FCA has also written to high street banks asking them to justify their lower savings rates, and threatened to take ‘onerous interventions’ if firms could not justify not passing on interest rates.

From the end of July, the FCA’s new Consumer Duty – a set of higher and clearer standards of consumer protection across financial services – will come into effect.

If it’s worth the paper it’s written on, it will lead to the regulator clamping down on firms that continue to set unjustifiably low rates for customers.

In the meantime, for savers currently unhappy with the deal they’re getting from their provider, our advice is simple – now’s the time to switch.

- Jenny Ross is the editor of Which? Money.